Housing Market Recovery Index Highlights – Week Ending July 18

- The U.S. housing market has recovered from the immediate disruption caused by the COVID pandemic and returned to January 2020 growth levels.

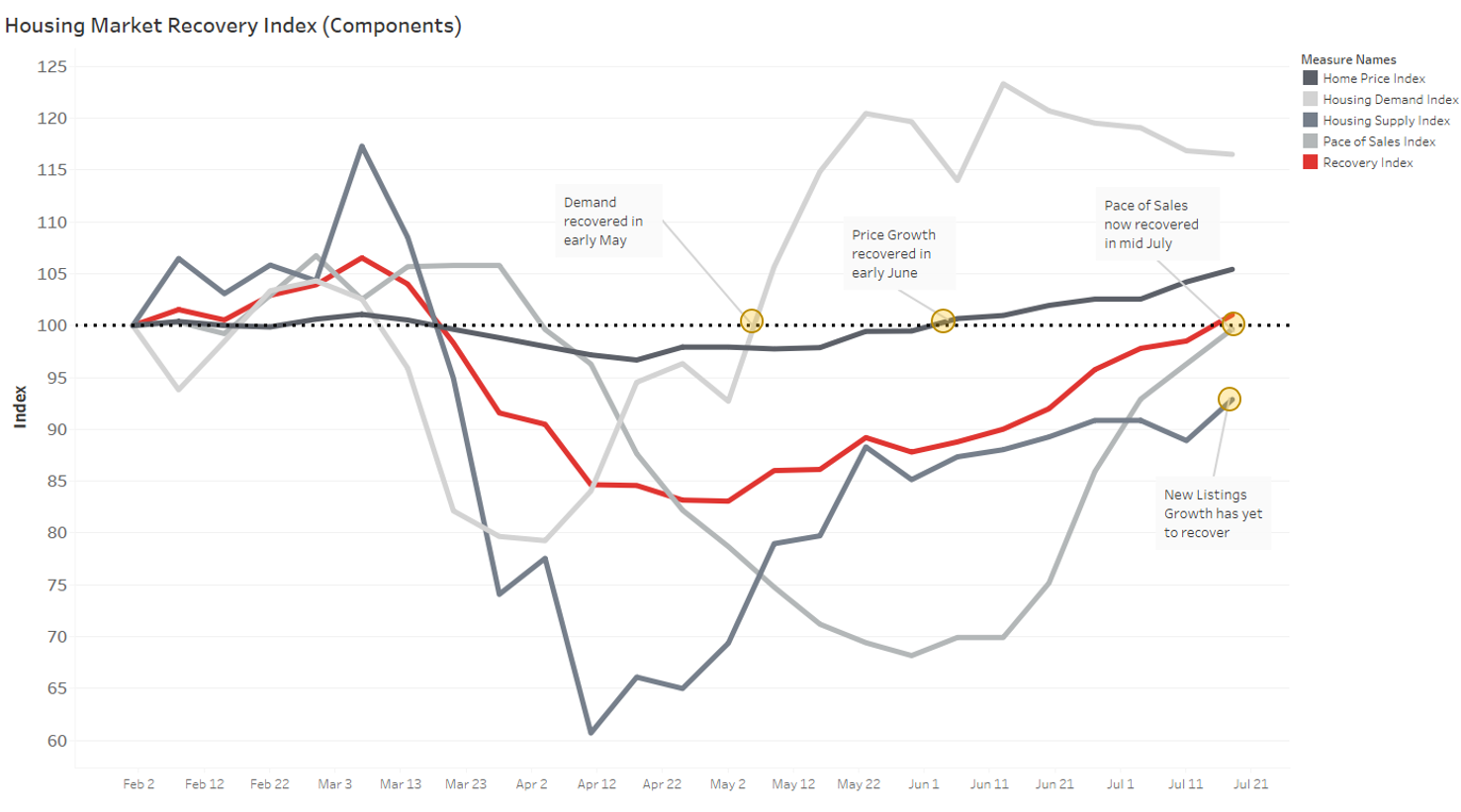

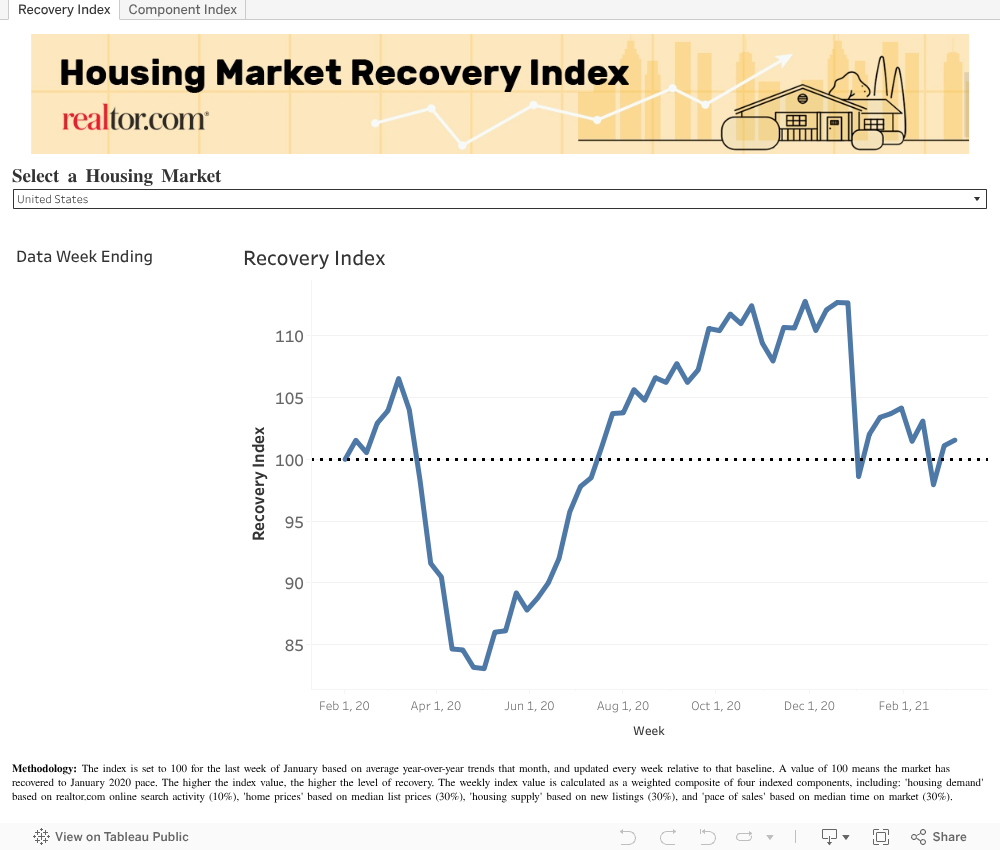

- The realtor.com Housing Market Recovery Index reached 101.0 nationwide for the week ending July 18, bringing the index above the pre-COVID recovery benchmark for the first time since March.

- The pace of home sales has now recovered with inventory moving faster than this time last year – but supply remains the critical missing piece in the recovery.

- The Northeast now leads the recovery with the overall index now visibly above the pre-COVID benchmark. The West (105.5) remains above recovery pace and continues to improve, while the South (97.9) and Midwest (97.3) are still lagging but regaining momentum.

- Half of the largest 50 markets in the country are now above the recovery benchmark, with the overall index showing greatest recovery in Boston, Seattle, New York, Philadelphia and Denver.

Download the full Housing Market Recovery Index dataset here.

National Recovery Trends

It’s taken four months for the U.S. housing market to get back to the more normal pace of growth we saw before the COVID-19 pandemic. The realtor.com Housing Market Recovery Index reached 101.0 nationwide for the week ending July 18, posting a 2.5 point increase over last week and bringing the index above the pre-COVID recovery benchmark for the first time since March.

The path to this initial point of recovery has been enthralling to watch and our index has provided the play-by-play each week. Demand from buyers was the first to recover in early May, followed by a price growth recovery in early June. Now, the pace of sales has caught up to pre-COVID levels too. Effectively, we’ve checked three of the four boxes of the housing recovery; supply remains the critical missing piece. Growth in supply remains below normal seasonal pace but continues to improve as buyers anxiously await for more sellers to put fresh new homes on the market.

There is no blueprint for a pandemic-induced recession, but this recovery milestone is further proof that homebuyers will persevere through the biggest of storms. Housing remains a must-have during COVID times, and home sales have proven to flourish even under record low levels of supply. The spring season disruptions have given an artificial boost to the summer homebuying season, and the pressure is now on the second half of the year to sustain that level of growth among eroding levels of inventory.

Effectively, this only marks the start of the recovery; another few months of sustained growth are needed to make up for lost ground in the first half of the year. An extended pandemic and economic aftershocks pose real short-term obstacles for housing. We may have crossed the recovery boundary once but the real question will be whether the market will be able to sustain that pace through the rest of the summer and going into the fall.

Notably, the pandemic and economic slowdown have not affected all housing markets equally. Half of large markets now sit above the recovery benchmark, but the gap between the most and least recovered has widened again. While no housing market will emerge unscathed, markets with superior COVID-19 containment and economic resilience have proven to be better positioned to withstand the bumpy road ahead.

| Week ending 7/18 | Current

Index |

w/w change | ||

| Overall Housing Recovery Index | 101.0 | +2.5 | ||

| Housing Demand Growth Index | 116.5 | -0.4 | ||

| Listing Price Growth Index | 105.4 | +1.2 | ||

| New Supply Growth Index | 92.9 | +4.0 | ||

| Pace of Sales Index | 99.7 | +3.4 |

The ‘housing demand’ component – which tracks growth in online search activity – remained visibly above recovery, with this week’s index reaching 116.5, down 0.4 points over the prior week. Despite showing signs of deceleration for the fifth week in a row, the demand index remains a healthy 16.5 points above the January baseline. The sustained, record-level homebuyer interest we’ve detected on realtor.com over the last two months has translated into higher activity this summer. Homebuyer sentiment appears to have fully recovered too, as lower mortgage rates have boosted consumer confidence. With supply levels low, this backlog of buyers portends increased competition and a shift toward a seller’s market.

Accordingly, the ‘home price’ component – which tracks growth in asking prices – increased by 1.2 points last week, and is now at 105.4, 5.4 points above the January baseline. With supply at record lows and buyer competition on the rise, sellers have regained leverage, enabling the fastest price growth recorded this year. As more offers come through this summer, we’ll get a good indication of whether higher asking prices will translate into higher selling prices. With supply limited, this is more likely.

Notably, the ‘pace of sales’ component – which tracks differences in time-on-market – saw continued signs of improvement for the fifth week in a row and is extremely close to the pre-COVID baseline. The time-on-market index reached 99.7, up 3.4 points over last week, and now just 0.3 points below the January baseline, suggesting buyers and sellers are connecting at a faster rate. However, further improvement in the pace of sales remains highly dependent on each market’s ability to contain COVID-19 and weather the economic impact.

The ‘housing supply’ component – which tracks growth of new listings – reached 92.9, up 4.0 points over the prior week and was 7.1 points below the January growth baseline. Sellers continue to be cautious, and further improvement could be constrained by lingering coronavirus concerns, and economic uncertainty going into the fall.

Local Recovery Trends

Northeast housing markets now leading the recovery – half of large markets now past recovery benchmark

Regionally, the Northeast (106.3) has overtaken all regions and now leads the recovery with the overall index now visibly above the pre-COVID benchmark. The West (105.5) remains above recovery pace and continues to improve, while the South (97.9) and Midwest (97.3) are still below recovery but regaining momentum in the recovery.

COVID-19 containment, and economic resilience are key factors driving regional differences in the housing recovery. The spread of COVID-19 is closely linked to the housing slowdown, with markets with higher cases per capita more likely to see a bigger impact on supply and the pace of sales. The speed and sustainability of the reopening, and each market’s ability to contain COVID-19, are dictating the speed of recovery across the regions. Finally, resilient economies may have an edge in the housing recovery, and areas with strong job markets before COVID-19, especially those with thriving tech sectors, are seeing buyers and sellers reconnect faster than the rest of the country.

| Region | Avg Recovery Index

(week ending 7/18) |

Weekly Change |

||

| West | 105.5 | +0.9 | ||

| South | 97.9 | +1.6 | ||

| Northeast | 106.3 | +3.7 | ||

| Midwest | 97.3 | +2.0 |

Half (25 of 50) of Large Markets Now Above the Recovery Benchmark

Locally, an additional seven markets have crossed the recovery benchmark this week, taking the total number of markets above the January baseline to 25, the highest since the early pandemic period. The overall recovery index is showing greatest recovery in Boston, Seattle, New York, Philadelphia and Denver, with the components of growth surpassing or approaching pre-COVID benchmarks. Markets in the sunbelt (Florida, Georgia, Louisiana, Alabama) with re-emerging COVID concerns and parts of the midwest (Michigan, Indiana, Wisconsin) with vulnerable economies are failing to see material improvements in recent weeks.

In the ‘housing demand’ component, 48 of the 50 largest markets are positioned above the recovery trend. The most recovered markets for home-buying interest include New York, Sacramento, Riverside-San Bernardino, Seattle and Buffalo, with a housing demand growth index between 133.3 and 138.5.

In the ‘home price’ component, more than half of markets are now positioned above the recovery trend, with 28 of the 50 largest markets seeing growth in asking prices surpass the January baseline, the same number as the previous week. In the top 10 most-recovered markets, asking prices are now growing at 11 percent year-over-year, on average. The most recovered markets for home prices include Pittsburgh, Cleveland, Louisville, Cincinnati, and Minneapolis, with a home price growth index between 106.2 and 113.4.

In the ‘pace of sales’ component, 27 of the 50 largest markets are now seeing the time on market index surpass the January baseline, up from 22 last week. In the top 10 most recovered markets for pace of sales, time-on-market is now down 14 percent, on average, year over year. Interestingly, markets where time on market is recovering the fastest tend to be faster moving than those with a slower recovery, suggesting seller markets pre-COVID may be better positioned for recovery in the months ahead. The most recovered markets for time-on-market include Boston, Philadelphia, Virginia Beach, Washington, and Rochester, with a pace of sales growth index between 115.9 and 132.8.

In the ‘housing supply’ component, 16 of the 50 largest markets saw the new listings index surpass the January baseline, up from 13 last week. Interestingly, markets where new supply was improving the fastest tended to be higher priced than those that had yet recovered, suggesting sellers were returning faster in the more expensive markets. The most recovered markets for new listings included Boston, San Francisco, Denver, Seattle and New York, with a new listings growth index between 120.9 and 131.5.

How to read the index – the overall index is set to 100 for the last week of January based on average year-over-year trends that month, and updated every week relative to that baseline. A value of 100 means the market has recovered to January 2020 pace. The higher the index value, the higher the level of recovery. The lower the index value, the lower the level of recovery.

Subscribe to our mailing list to receive monthly updates and notifications on the latest data and research.